Market Backdrop

Housing turnover remains the single biggest demand driver for flooring, and it remains below historical norms. Existing home sales reached 4.09 million units in February, with inventory at its highest level since 2019. This signals early signs of stabilization, not further contraction.

The more important story is what is building underneath: homeowners who paused renovation plans haven't cancelled them. They've waited. As inventory loosens and life events force decisions, that backlog will convert. The retailers positioned to capture it are the ones investing in digital visibility now.

What Buyers Are Searching For

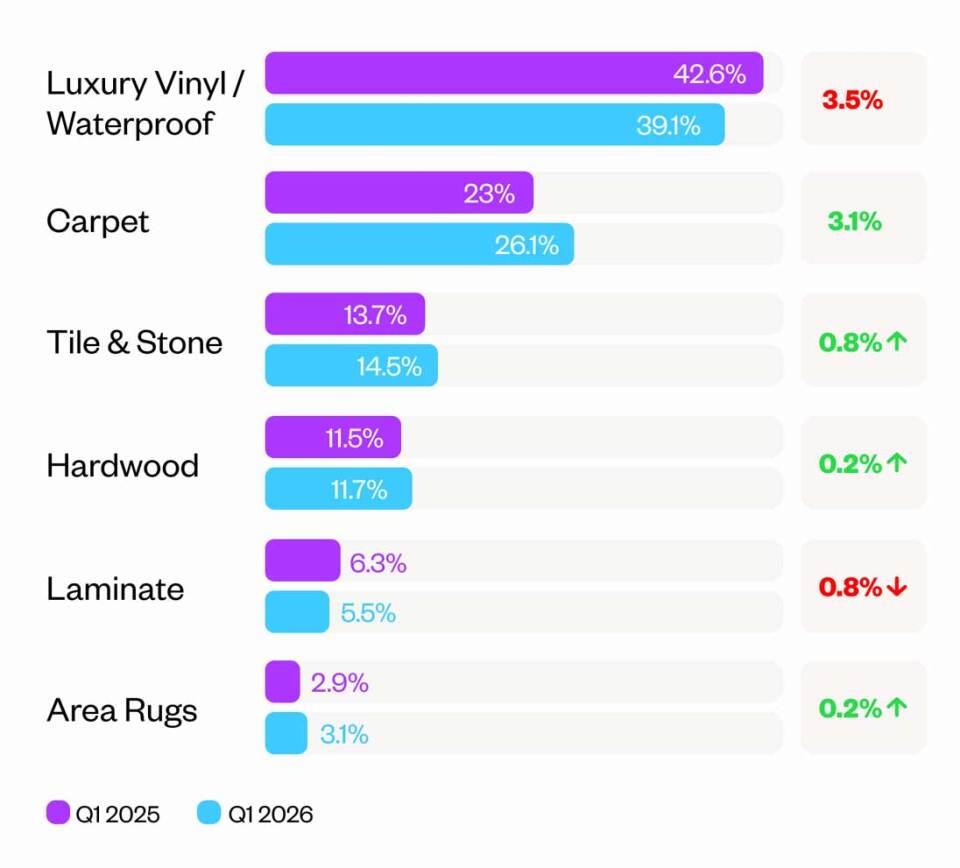

Luxury Vinyl / Waterproof remains the most-browsed category at 39.1% of all product views, but lost 3.5 percentage points of share year over year.

Carpet is the only major category to gain significant share (+3.1pp), now at 26.1% of all product views.

Laminate is the steepest absolute decliner, with 5.5% of raw views and down 0.8pp of share.

Tile & Stone and Hardwood are holding steady as an overall share of products viewed.

Total category page views declined 14.3% year over year, consistent with broader market softening.

Action Items

Homeowners who paused renovations haven't cancelled, they've just waited. When confidence stabilizes and housing activity picks up, that backlog will convert. Retailers with a strong digital presence and CRM tools to manage and nurture leads will be the first call when a homeowner is ready to move.

Form submissions held up far better than phone calls this quarter – buyers are doing more research online before they’re ready to talk. An up-to-date product catalog, clear navigation, and current content earn a shopper’s confidence before the first conversation begins.

Blog articles about care, installation, and flooring trends appeared among the most-visited pages across our network. Practical, helpful content captures buyers at exactly the moment they have a question – and routes them toward the retailer who answered it.